市场摘要:一个平静的交易日,投资者们在期待本周晚些时候的FOMC利率决议,全天小幅上涨将标普500 指数推高至历史高点咫尺之遥,而道琼斯指数则创下其历史新高。随着主要科技股的下跌,纳斯达克指数在交易日结束时小幅回落,主要原因为苹果公司的下跌,由于几位分析师指出可能有迹象表明苹果手机的销售放缓。人工智能板块也在英伟达的带动下走低。能源板块因油价上涨而表现出色。

亚洲夜间期货交易清淡,日经指数和 Kospi 指数因中秋节休市,香港和中国市场变化不大。

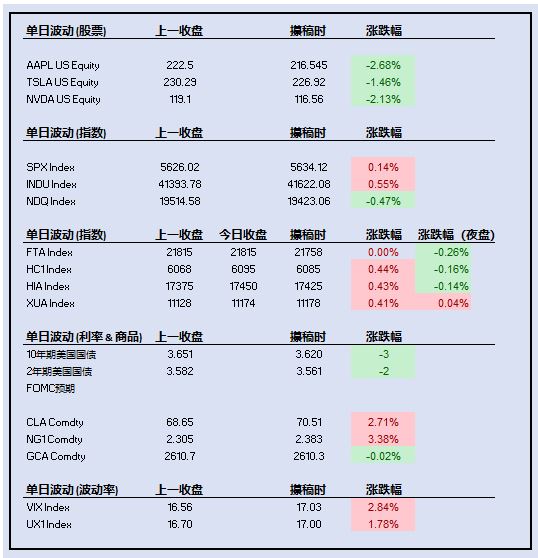

Market Highlights On a quiet trading day, investors are anticipating the FOMC rate decision later this week, with small gains for the day pushing the S&P 500 within an inch of the all-time high, while the Dow Jones did post an all-time high today. With declines in the main technology names the Nasdaq ended the trading day with a small retreat, driven among others by Apple as several analysts pointed towards possible signs of slowness in i-phone sales. The Artificial Intelligence sector was also lower, led by Nvidia. The energy sector outperformed on the back of higher oil prices.

In Asian night futures trading, action was light with Nikkei and Kospi closed for the Mid-Autumn Festival, while Hong Kong and China markets were little changed.

主要股指:标普500涨0.14%至5,634.12;道琼斯涨0.55%至41,622.08;纳斯达克100跌0.47%至19,423.06。

美市个股:苹果跌2.68%至216.55美元;特斯拉跌1.46%至226.92美元;英伟达跌2.13%至116.56美元。

亚洲指数自各市场收盘后:日经225期货中秋节休市;韩国Kospi200期货中秋节休市;恒生指数期货跌25点至17,425(跌0.14%);恒生国企指数期货跌10点至6,085(跌0.16%);富时中国A50期货涨4点至11,178(涨0.04%)。

利率与预期:10年期美国国债利率跌3基点至3.62%;2年期美国国债利率跌2基点至3.56%;周三 FOMC 会议上“巨幅“降息 50 个基点的预期升至 65%,大多数人对年内降息幅度的预期升至 125 个基点(45%)。

外盘商品:原油期货涨2.71%至70.51美元;天然气期货涨3.38%至2.383美元;黄金期货跌0.02%至2,610.30美元。

波动率:现货收于17.03(涨0.47点);VIX 期货(合约期9月)收于17.00(涨0.30点);标普500指数1个月平价隐含波动率收于13.8%(基于相同行权价涨0.2点);纳斯达克100指数1个月平价隐含波动率收于19.5%(基于相同行权价跌0.1点)。

【注:此处的任何内容均不构成购买证券的要约或要约邀请。】

$TRUE PARTNER(HK|08657)$

数据源自芝加哥时间2024年9月16日下午16时Bloomberg (平价波动率数据源自True Partner)。

本文作者可以追加内容哦 !